SAN FRANCISCO REAL ESTATE MARKET UPDATE

June 1, 2023

HELM Newsletter

June 1, 2023

HELM Newsletter

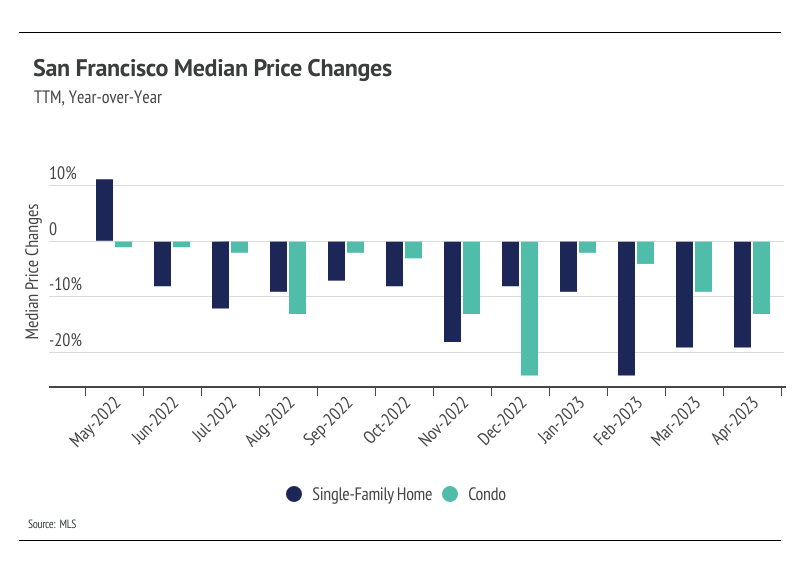

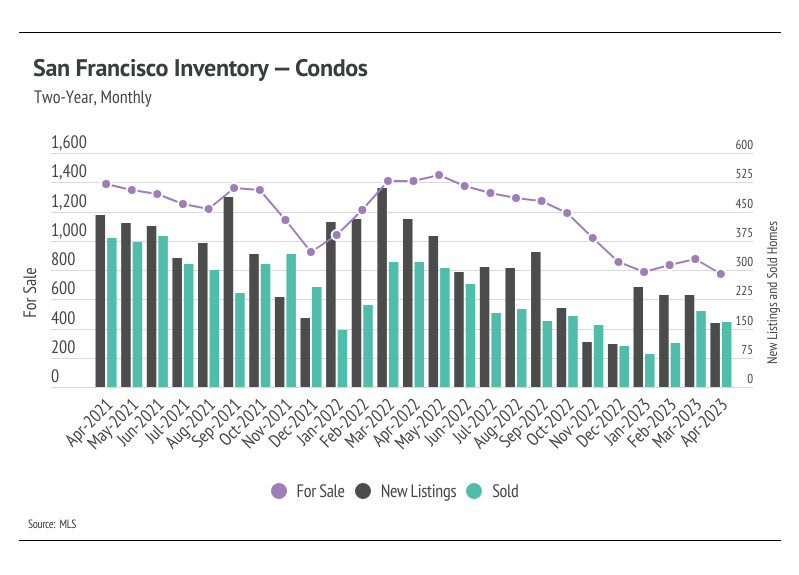

Inventory is near historic lows in San Francisco. For single-family homes, inventory and new listings declined from March to April, while sales increased. Sales as a proportion of active listings increased month over month for single-family homes, further highlighting the increasing demand. The condo market, however, saw declines across all three metrics month over month, but inventory is so low that a dip in sales doesn’t necessarily imply softening demand. The number of home sales is, in part, a function of the number of active listings and new listings coming to the market. Even with higher interest rates, which only reduces the number of potential homebuyers, seasonal demand far outpaced available inventory. Over the past three months, total sales jumped 100% while new listings declined 26%. Inventory will almost certainly remain historically low for the year and will likely only get more competitive in the summer months.

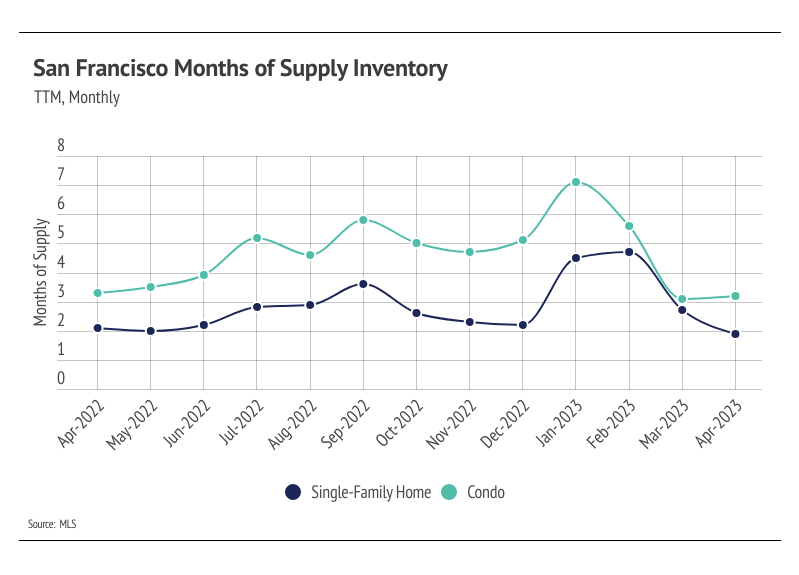

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI declined over the past three months for both single-family homes and condos, indicating that the climate has shifted from a buyers’ market to a sellers’ market for single-family homes and a balanced market for condos. The sharp drop in MSI occurred due to the higher proportion of sales relative to active listings and less time on the market.

If you are interested in selling, buying or just curious about the

San Francisco and Bay Area real estate market, please give me a call.

We are here to help you and anyone you care about.

Stay up to date on the latest real estate trends.

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

BUSINESS

September 1, 2025

BUSINESS

August 1, 2025

BUSINESS

July 1, 2025

You’ve got questions and we can’t wait to answer them.