SAN FRANCISCO REAL ESTATE MARKET UPDATE

March 31, 2023

HELM Newsletter

March 31, 2023

HELM Newsletter

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

_________________________

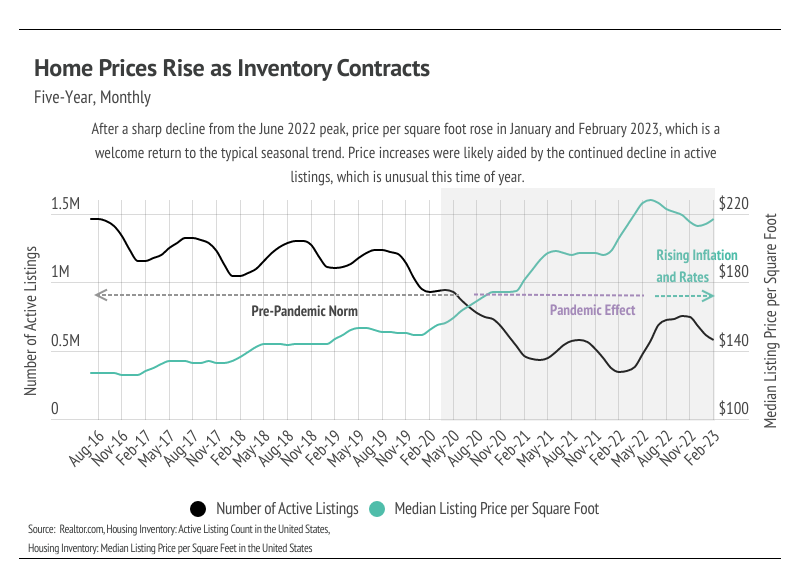

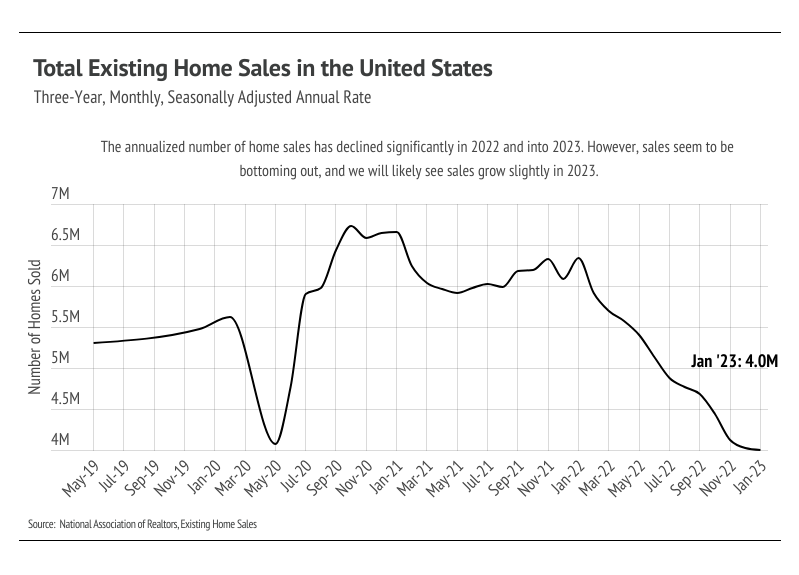

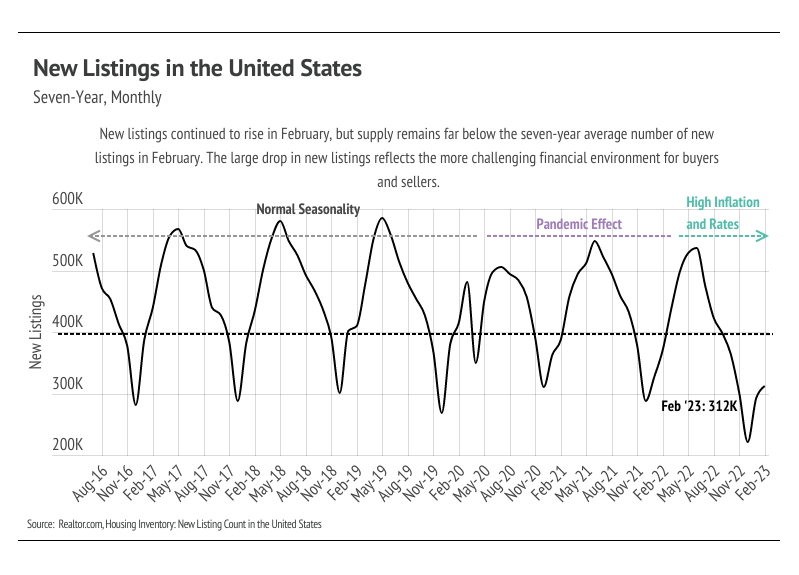

This time of year, we usually see both inventory and sales increasing steadily through mid-summer. Inventory is able to grow, even with rising sales, because of the relatively high number of new listings that typically come to market in the first half of the year. However, the number of new listings decreased from January to February, which is an early sign that inventory will struggle to grow this year. Although we expect sales to be more muted this year, demand could start to outpace supply, especially if sales continue to rise without being met by more new listings. For now, rising mortgage rates have dampened demand enough that supply isn’t an issue. Higher mortgage rates tend to hit more expensive markets much harder than less expensive markets, unless a significant amount of the property is paid for in cash, due to the absolute dollar cost of financing. For example, a $500,000 30-year mortgage at 6.5% is much more affordable ($3,160 per month) for many more potential buyers than a $1 million mortgage at 6.5% ($6,321 per month).

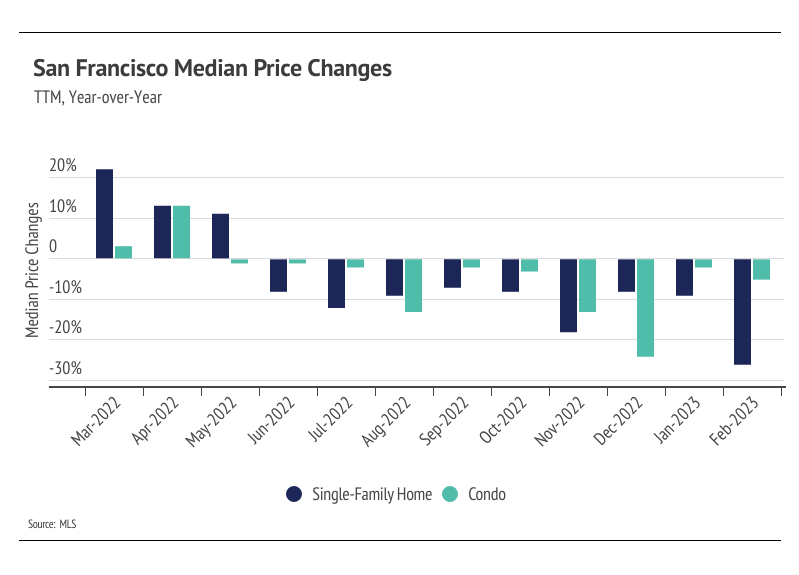

As one of the most expensive markets in the country, San Francisco real estate prices have been hit harder than other markets. Single-family home prices have declined 10.6% over the past two years after declining 28.9% from the March 2022 peak. Condo prices have only declined 13% from the April 2022 peak, which brought prices to the same level as February 2021. The next three months will give us a clearer picture of how buyers and sellers are reacting to the current market conditions, but early signs point to more competition over the limited number of listings in San Francisco as we enter the spring season.

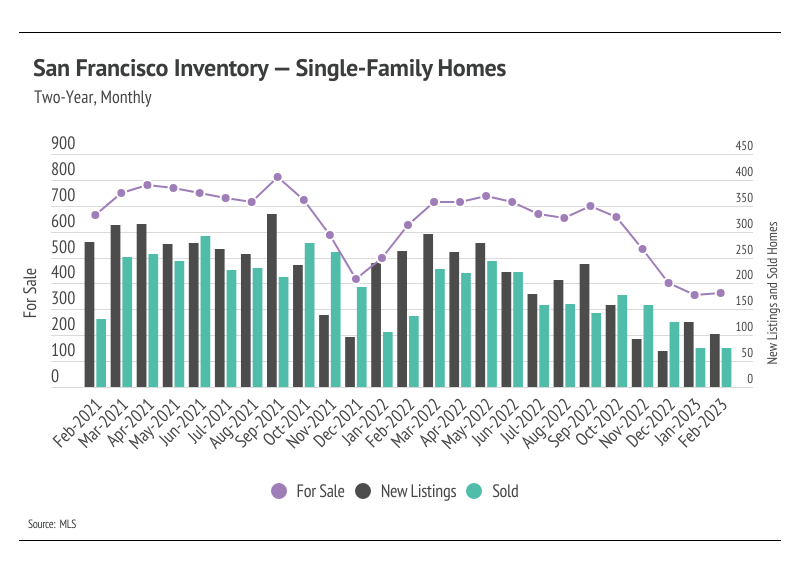

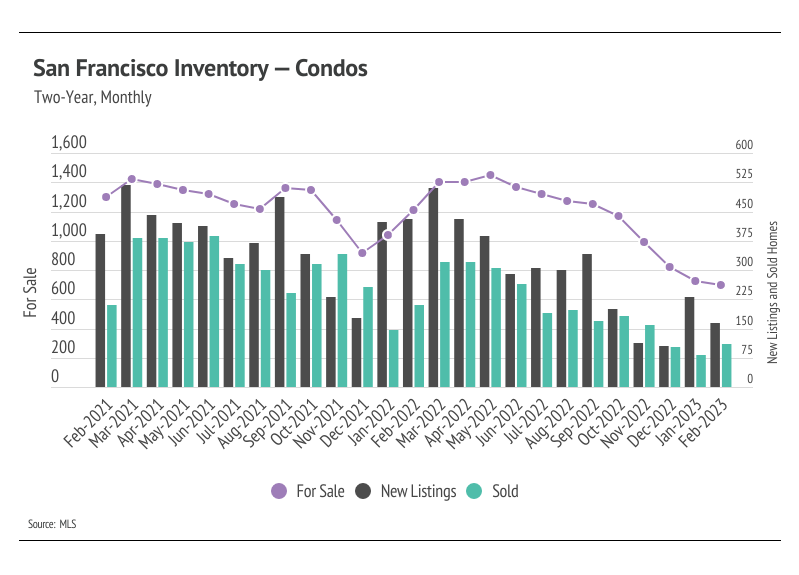

Single-family home inventory rose slightly month over month, as new listings outpaced sales. Condo inventory fell further as sales increased and new listings decreased. Higher interest rates have dropped incentives for potential sellers to enter the market, since sellers usually also must buy a new home. Homeowners either bought or refinanced recently, locking in a historically low rate, which means they aren’t selling and fewer listings are coming to market. Moreover, many potential buyers were priced out of the market as interest rates rose; however, interest rates have been higher for enough time that buyers are more comfortable re-entering desirable markets like San Francisco. Currently, buyers aren’t facing anything similar to the hypercompetitive 2021 market, but we will likely start to see a more competitive market in the spring. New listings fell by 60.9% year over year, while sales declined 45.8%. We still expect some inventory growth in the first half of 2023, but inventory will likely remain low.

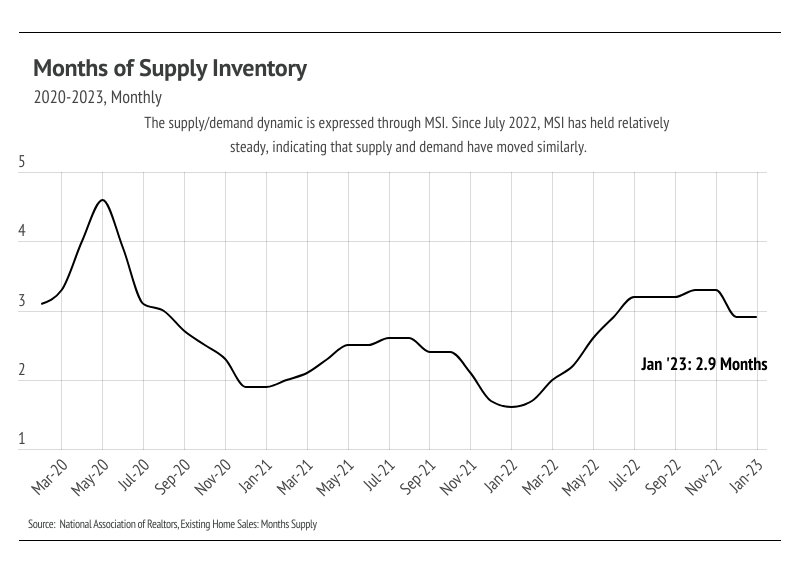

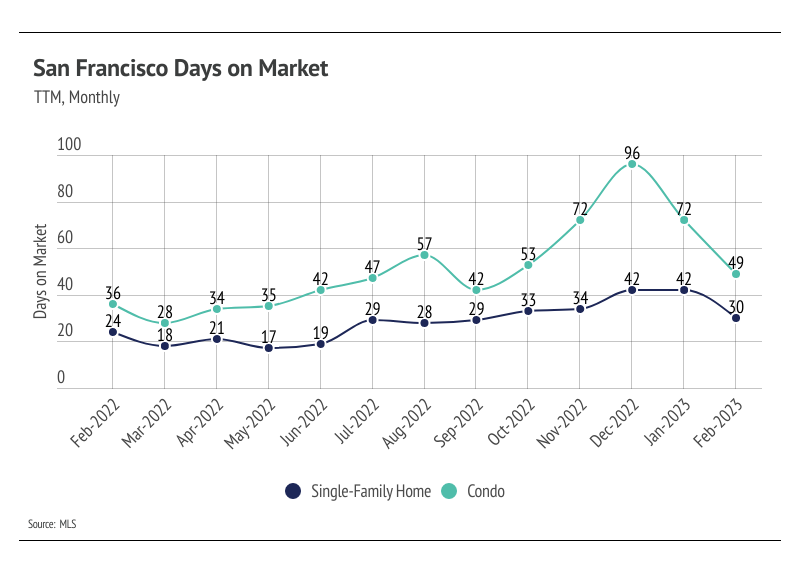

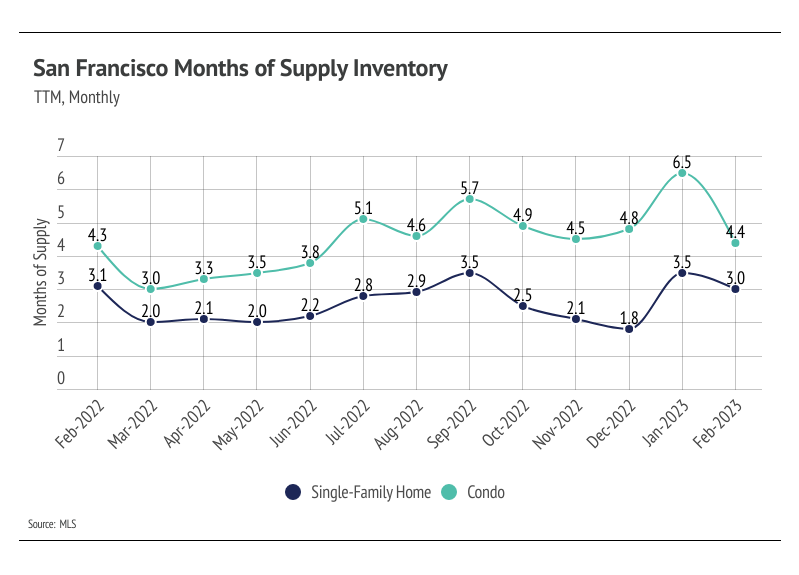

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). MSI dropped in February for both single-family homes and condos, indicating the market is starting to get more competitive. The sharp drop in MSI occurred due to homes selling more quickly and fewer new listings coming to market. Currently, MSI implies a balanced market for single-family homes and a buyers’ market for condos.

If you are interested in selling, buying or just curious about the

San Francisco and Bay Area real estate market, please give me a call.

We are here to help you and anyone you care about.

Stay up to date on the latest real estate trends.

BUSINESS

July 1, 2026

BUSINESS

June 1, 2026

BUSINESS

May 1, 2026

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

You’ve got questions and we can’t wait to answer them.