SAN FRANCISCO REAL ESTATE MARKET UPDATE – June 2020

June 1, 2020

Real Estate

June 1, 2020

Real Estate

A Message from Our Crew to Yours

We hope this message finds you healthy. Our crew is committed to continuing to serve all your real estate needs while incorporating safety protocol to protect all of our loved ones.

We also want to assure you that of all investments you can make, real estate has historically proven to be the best asset you can own in the long-term. As we all navigate this together, please don’t hesitate to reach out to us with any questions or concerns. We’re here to support you.

– Your HELM Crew

_________________________________________________________________________________

__________________________________________________________________________________

Key News and Trends Impacting Your Local Market

April home and condo prices rose in San Francisco on both a monthly and yearly basis. Even more surprisingly, home and condo prices fell only slightly statewide. In April, California median home prices declined 1% according to the California Association of Realtors (CAR).

As a general rule of thumb, homeowners benefit from refinancing if they can lower their rates by at least 1%. Refinancing also provides an opportunity to dispense with private mortgage insurance (PMI), as long as the value of the home has risen and the owner has enough equity in the home.

For owners of Q1 2020 median-priced California homes ($612,000), a 1% reduction would reduce monthly payments by $300. The savings for a median-priced home in San Francisco ($1.7 million) is around $800 per month. Refinancing, however, comes with costs, which include title insurance, attorney’s fees, the price of an appraisal, taxes, and transfer fees, among others. Expect refinancing to run anywhere between $1,500 and $5,000. While most costs are fixed, appraisals are variable and cost more for larger homes.

The second biggest determinant of whether or not to refinance, therefore, is whether or not the homeowner plans to stay in the home long enough to recoup the costs of refinancing. For instance, if refinancing costs $4,000 and the homeowner stands to save $800 each month on their mortgage payment, then their costs will be recouped after five months of living in the home. As a result, the homeowner would benefit from refinancing if they plan to stay in the home for longer than five months.

Due to the large cost savings and short breakeven period for refinancing, the number of refinance eligible borrowers—borrowers paying interest 0.75% or higher than current rates with credit scores above 720 and enough equity to get a new loan—rose to 11.3 million, the second-highest on record, according to Black Knight.

For homeowners looking to sell rather than refinance, technology continues to change how the real estate market operates.

Stay-at-home orders make video calling a daily activity, which has quickly increased the overall comfort level with technologies like Zoom, Skype, and FaceTime across demographics. 3D virtual tours have become commonplace over the last several years, but they are even more important now. Video call showings are becoming more normalized with each passing day. Exact data on the increase in agent-led virtual tours is difficult to gather with an MLS, but in March, CNBC provided some color using data from Zillow and Redfin. Zillow showed a 191% increase in the creation of 3D virtual home tours in the first week of March compared to February, and Redfin’s requests for agent-led video tours increased 94x from the first week of March to the last. Because of the rapid adoption and comfort with video technology, we expect the market to normalize relatively quickly, bringing sales volumes and inventory back to more typical seasonal trends and helping restore a more balanced market.

_______________________________________________________________________________________

May Housing Market Update for San Francisco

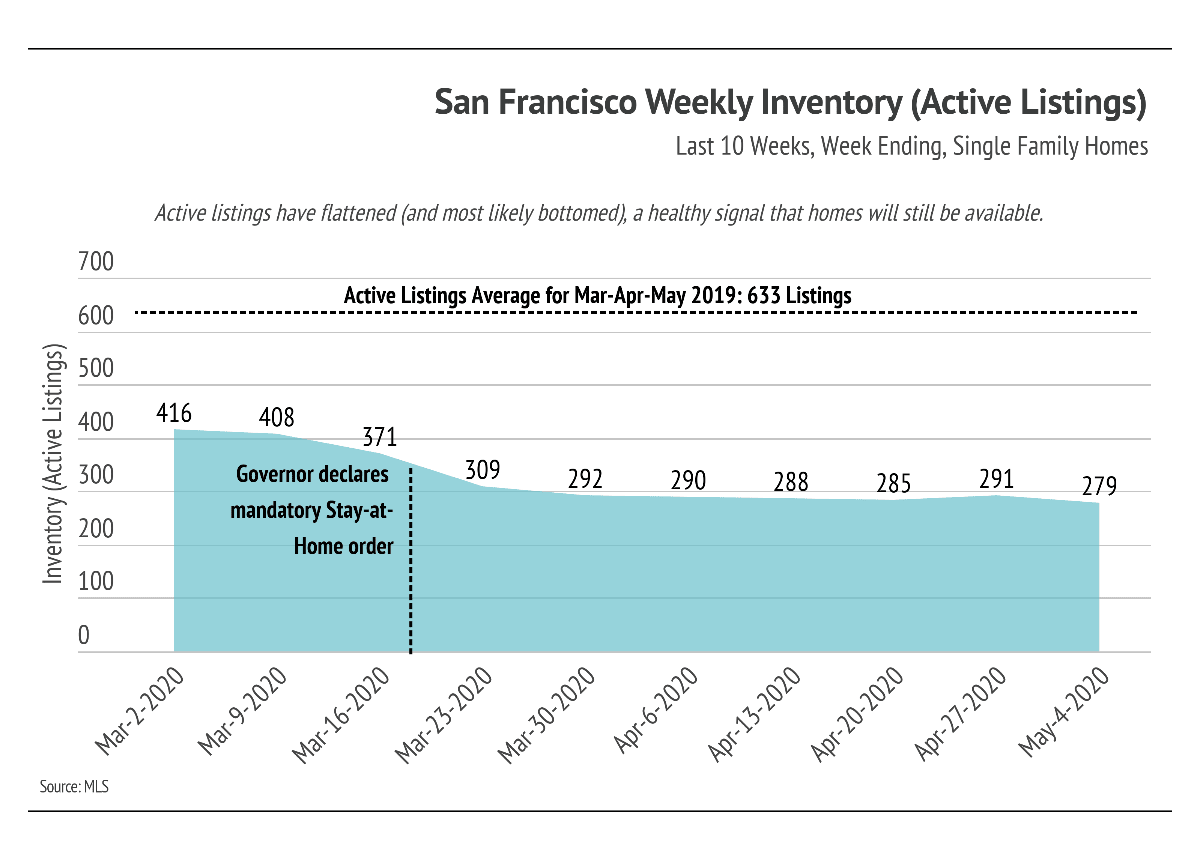

While the pandemic’s impact on the housing market progressed rapidly in March, the April housing market data illustrates a stable market, albeit at a new normal. The graph below illustrates the available housing inventory by week rather than by month (as is typical) to illustrate how the market has changed over a shorter timeline. We can see that supply levels declined in March, but have since flattened. A significant number of sellers continue to remain in the market, and this so-called floor might indicate that active listings have fallen as far as they will go.

Another sign that the housing market may be beginning to turn around is the number of listings under contract. During the week of March 30th, listings under contract hit a low with only 11 single-family homes under contract. Since then, listings under contract are almost three times that amount (31), indicating that people are forging ahead, aided by technology.

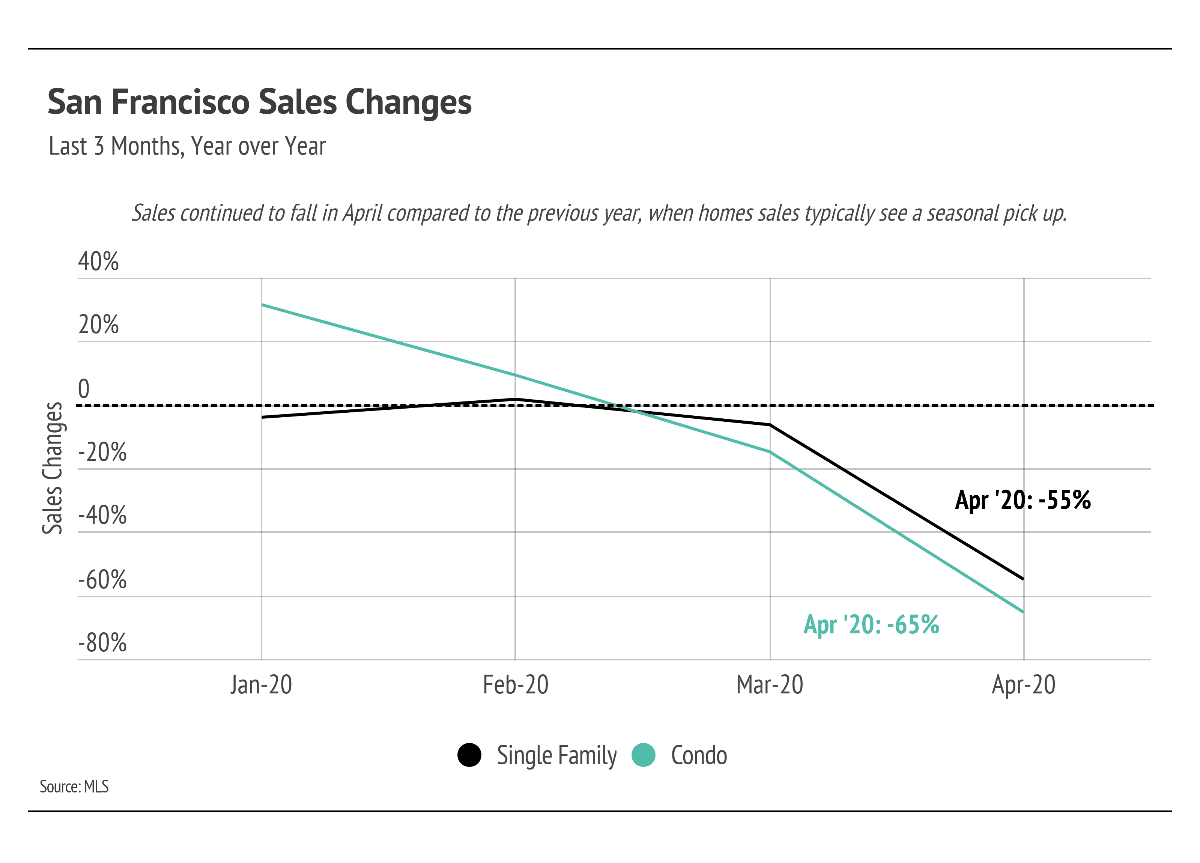

As discussed earlier, San Francisco’s median prices rose in April for both single-family homes and condos. Although the pandemic and stay-at-home orders dampened buyer demand, the number of active listings also decreased, which buoyed prices.

Compared yearly, prices were up for both single-family homes and condos as well. Appreciating prices typically signal a healthy demand for the available housing and encourage sellers to price their homes slightly above comparables.

Along with a rise in median home prices, the percentage of homes that sold with price cuts remained at the lowest level in the past ten months. Only 7% of sellers had to reduce their prices in April. Rising price data will only encourage sellers to keep their listings priced where they are and wait for more buyers to come back into the market.

The sale-to-list ratio reflects the change in the original list price of a home and the final sale price. For example, a ratio of 100% means that a home sold for the price at which it was most recently listed. In San Francisco, single-family homes almost always have higher sale-to-list ratios than condos. In April however, single-family home sellers accepted offers at a discount for the first time in over a year. This indicates that sellers are finally making price concessions, albeit small ones, and that buyers have a bit more negotiating power. Meanwhile, sale-to-list ratios rose for condos; buyers paid a 4% premium. It’s important to note that the sample size for April sales is over 50% smaller than usual, making this month’s metrics outliers rather than the start of a new trend. We will, of course, continue to track this metric in order to guide your decision making.

Inventory and volume of homes sold saw a significant decrease in March and April. The year-over-year changes are particularly pronounced as sales and inventory typically have a seasonal increase in March and April, coming out of the slower Winter season.

Looking to June, we anticipate more growth. We expect buyer demand to pick back up as fears of a steep price decline lessen. Look for more agents to leverage the latest technology to give buyers the ability to tour homes in compliance with state and local laws.

As we discussed in previous newsletters, the fundamentals of the housing market were strong before the global economy stalled, which we believe will help us all navigate this difficult time with as little consequence to the market as possible.

As always, we remain committed to helping our clients achieve their current or future real estate goals. Our team of experienced professionals would be happy to discuss the information we’ve shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

Stay up to date on the latest real estate trends.

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

BUSINESS

September 1, 2025

BUSINESS

August 1, 2025

BUSINESS

July 1, 2025

You’ve got questions and we can’t wait to answer them.