SAN FRANCISCO REAL ESTATE MARKET UPDATE – July 2022

August 18, 2022

BUSINESS

August 18, 2022

BUSINESS

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

_________________________

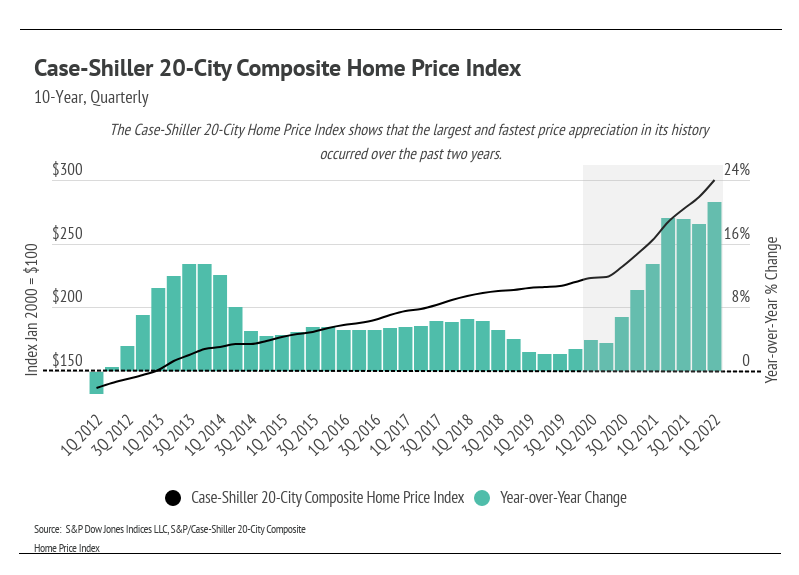

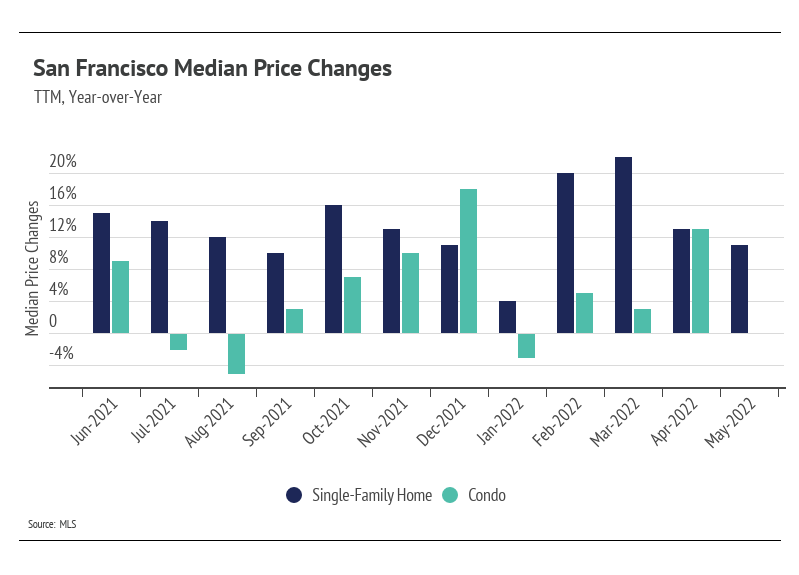

In May, home prices increased around 16% year-over-year, which means that prices would double every 4.5 years if that trend were to continue. That kind of rapid growth is simply unsustainable and would eventually lead to a major market collapse. Based on what happened as a result of the 2006 housing bubble, we know that mass wealth destruction is not the path we want to take. The Federal Reserve (the Fed) is actively raising rates to bring down the growth rate by making borrowing more expensive, thereby lowering demand. Luckily, we are starting to see inflation respond to the Fed’s monetary policy, although it is still near a 40-year high.

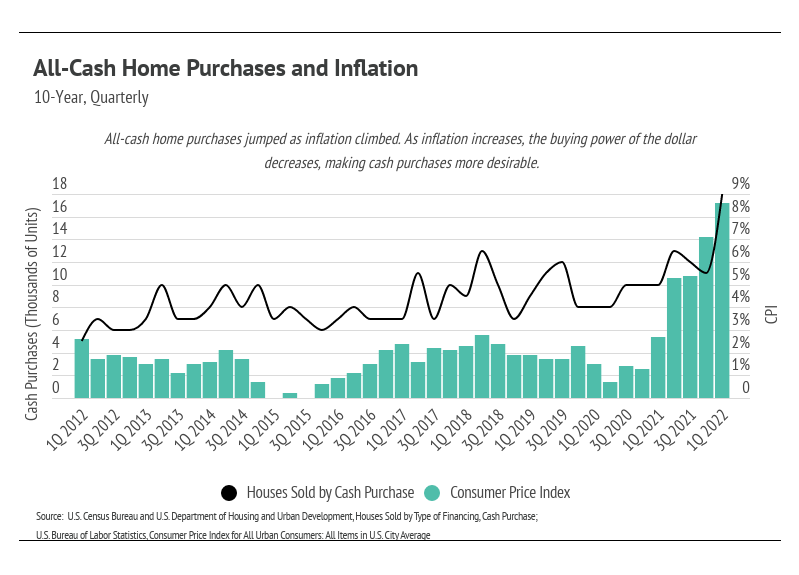

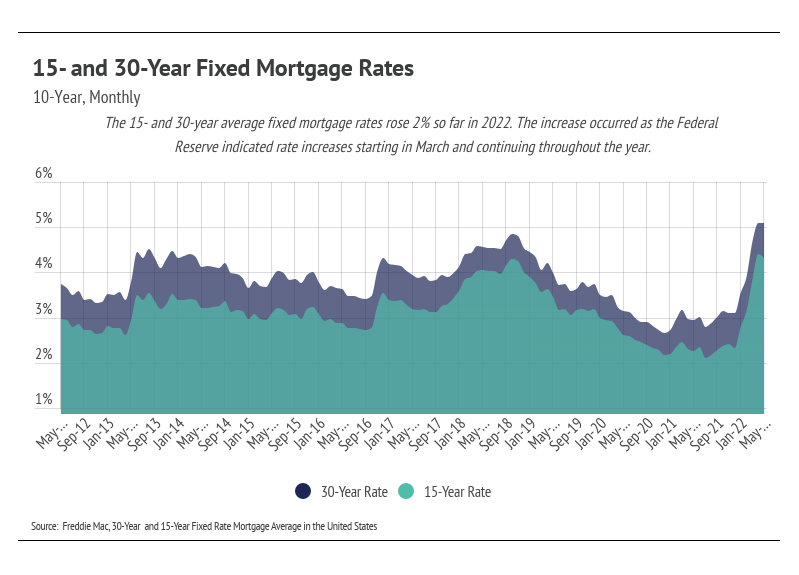

In 2022, mortgage rates have moved about 2% higher for 30- and 15-year fixed mortgages, reaching 5.09% for the average 30-year fixed-rate mortgage and 4.32% for the average 15-year fixed-rate mortgage as of June 2, 2022. Every 1% rate increase raises the monthly mortgage payment significantly — by about 13%. In this environment of rising rates and rising inflation, all-cash purchases become more attractive because financing is more expensive and money is worth less over time. In the first quarter of 2022, all-cash purchases increased, reaching the highest levels since 1988. Economists now estimate that the average 30-year mortgage rate could climb above 6% in 2022. Because the Fed indicated the path of rate hikes for the rest of the year, we expect that mortgage rates will, at most, reach around 7% this year for prime borrowers.

If it feels like you missed a unique opportunity to finance a home at under 5%, we are sorry to say that you did. However, you are in good company and can still take advantage of low rates. While it can feel like rates are high when they’ve risen from the all-time low of only a few months earlier, a rate of 5% is still historically low. Since 1971 (the start of the data set), we’ve had 2,671 weekly 30-year mortgage data points, only 24% of which reflected rates below 5%.

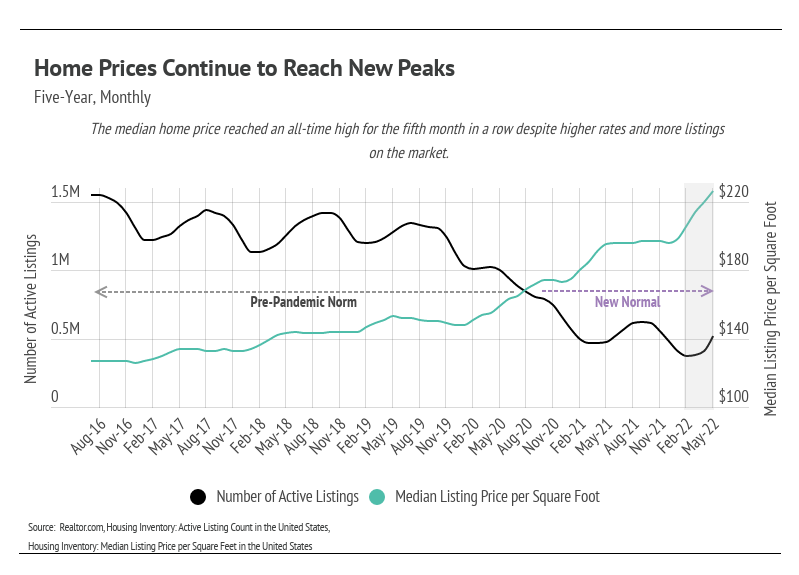

The market has remained so hot because of supply — or lack thereof. In May, the housing supply ticked up ever so slightly but is still 49% lower than the number of homes on the market in May 2020. We are entering what is traditionally the hottest time of year for the housing market with a record low supply of homes. Through May 2022, which had the lowest inventory on record, home prices increased 15%. The chief economist at Realtor.com, Danielle Hale, explains that the market is about 5.8 million single-family homes short, which means we’re four to five years behind in building new homes. Although single-family housing starts — homes that have begun construction — have slowed recently, multi-unit housing (5+ units) starts have reached their highest numbers since 1986.

|

|

|

|

|

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

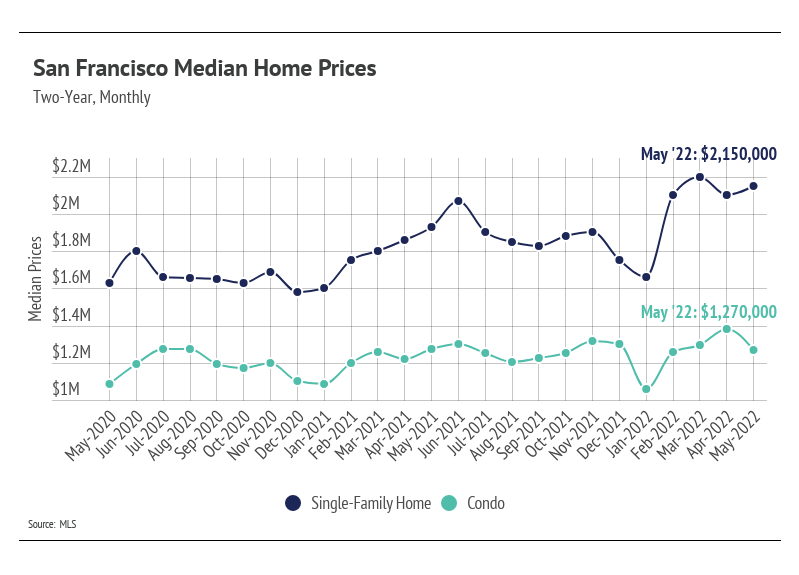

Home prices continue to rise as new listings meet the high demand

The median single-family home price rose in May, landing just below the all-time high reached in March, while the median condo price declined from the April peak. Rising rates haven’t brought down home demand so far, and in a rising rate environment, buyers are better off locking in an interest rate sooner rather than later. Since the start of 2022, the average 30-year mortgage rate has increased by 2%, which equates to a 27% increase in monthly mortgage payments. Yet prices keep moving higher.

One reason that home prices continue to rise is that buying a home is not only a financial process but also an emotional one. Over the past two years, our homes have become such a large part of our lives, with many of us moving to permanently remote or hybrid work. As more homes come to the market, as is typical in the first half of the year, buyers are more likely to find the home that’s right for them in what’s been an incredibly competitive market. Even with increases in mortgage rates (which, again, are still historically low), it’s reasonable to pay more for the well-being that comes with buying the right home. For most of us, our home is our largest asset and store of wealth, so treating it as such makes sense.

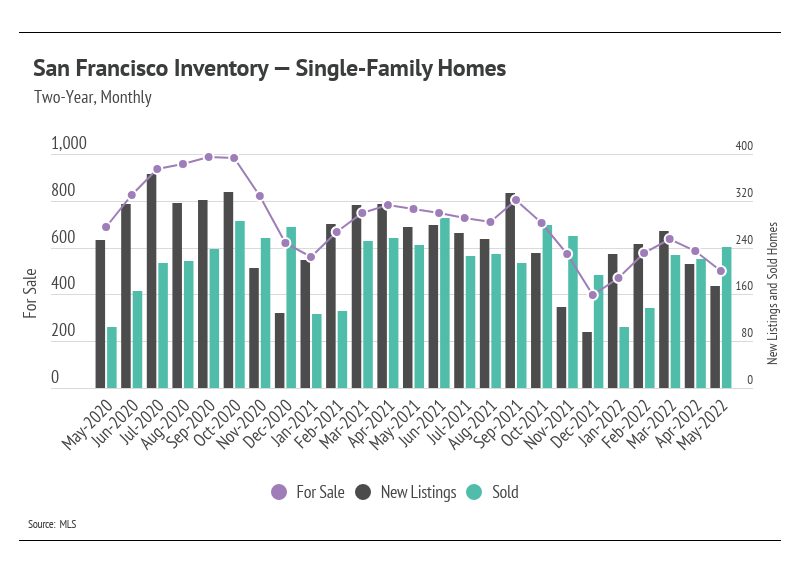

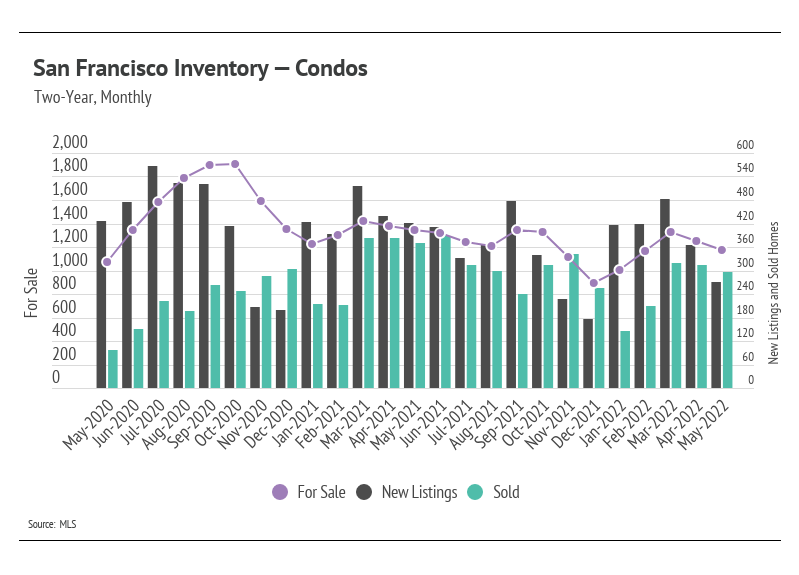

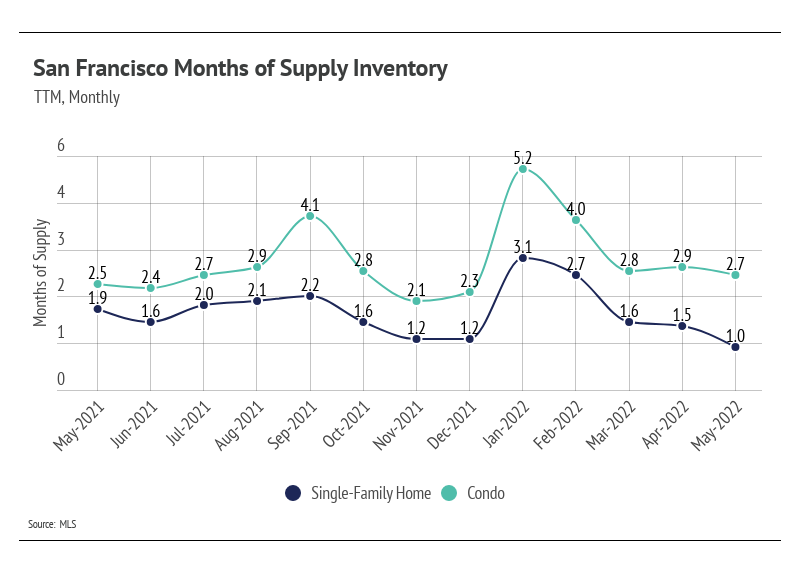

Declining inventory, way ahead of schedule

San Francisco’s housing inventory declined in May for the second month in a row, which serves as an early indicator that home supply will remain significantly depressed this year. The high demand and lack of new listings over the past year brought single-family home and condo supplies to record lows as we entered 2022. Although the first quarter of 2022 had one of the lowest inventories on record, we were pleased to see that inventory increased, a trend that usually holds until mid-summer. But with inventory reversing in April and May, the likelihood of a strong inventory increase is slim.

Even though inventory is low, sales remain relatively high, outpacing new listings for both single-family homes and condos. Sellers can expect multiple offers, and buyers should come with competitive offers.

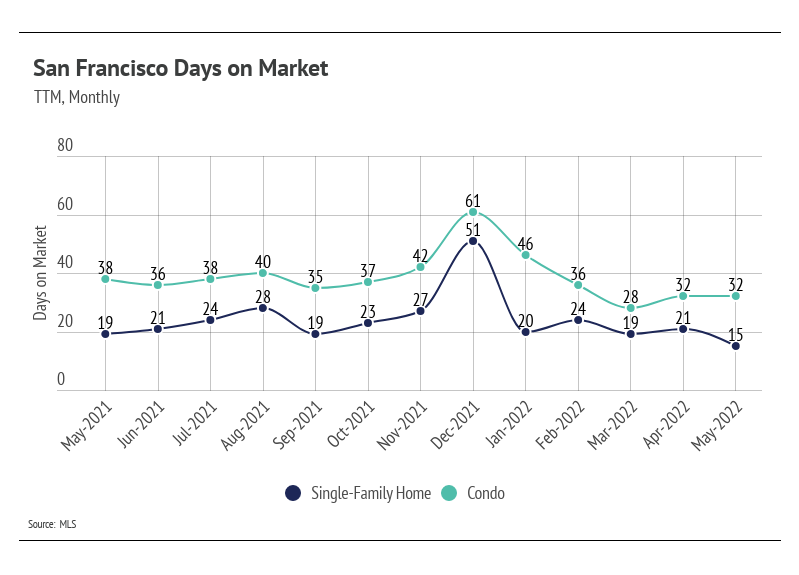

Months of Supply Inventory further indicates high demand and low supply

Homes are selling faster than ever. Buyers must put in competitive offers, which, on average, are 14% above the list price for single-family homes and 6% above the list for condos.

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). Currently, single-family home and condo MSIs are low, indicating a strong sellers’ market.

|

|

|

|

|

|

_________________________

If you are interested in selling, buying or just curious about the

San Francisco and Bay Area real estate market, please give me a call.

We are here to help you and anyone you care about.

_________________________

Stay up to date on the latest real estate trends.

BUSINESS

June 1, 2026

BUSINESS

May 1, 2026

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

BUSINESS

September 1, 2025

You’ve got questions and we can’t wait to answer them.