SAN FRANCISCO REAL ESTATE MARKET UPDATE – October 2020

October 1, 2020

Real Estate

October 1, 2020

Real Estate

In this month’s newsletter, we cover the following:

______________________

Key Topics and Trends in September

The pandemic tested the efficacy of large-scale remote work, causing companies to reconsider the need for massive office spaces. Notably, Pinterest announced in late August 2020 that it paid $89.5 million to terminate its lease on a yet-to-be-built 490,000 square foot office space. The choice reflects Pinterest’s reevaluation of its workforce needs, and its realization that more employees can work from home on a regular basis. Pinterest is showing another “new normal” for companies: hiring employees from different parts of the country without requiring those employees to relocate near the office. As a result, companies and employees are even less restricted by geographic location than they ever have been in the past.

SFGate reports that San Francisco is not going through an abnormal population exodus; rather, San Francisco simply is not seeing the usually high number of people moving to the city. The effect remains mostly the same in that there is less renter demand, which has caused one-and two-bedroom apartment prices to drop around 15% year-over-year.

Although fewer people moving to the city sounds like it would lower the demand for homes and, therefore, decrease home prices, the median home price has actually remained stable through August. In order to explain why prices have not changed, we can look to affordability. According to the California Association of Realtors, a median homeowner needs to earn a minimum income of $322,000 and be able to pay $8,000 per month for mortgage, taxes, and insurance. This type of wealth is far different than the average renter, who now pays less than $3,000 per month.

Unlike many other cities around the country where the cost of a mortgage is similar to the cost of rent, San Francisco maintains a large gap between those that can afford rent versus those that can afford a mortgage. The rental market, which is receiving a lot of press for its steep decline, does not foreshadow a decline in single-family home prices.

______________________

September Housing Market Updates for San Francisco

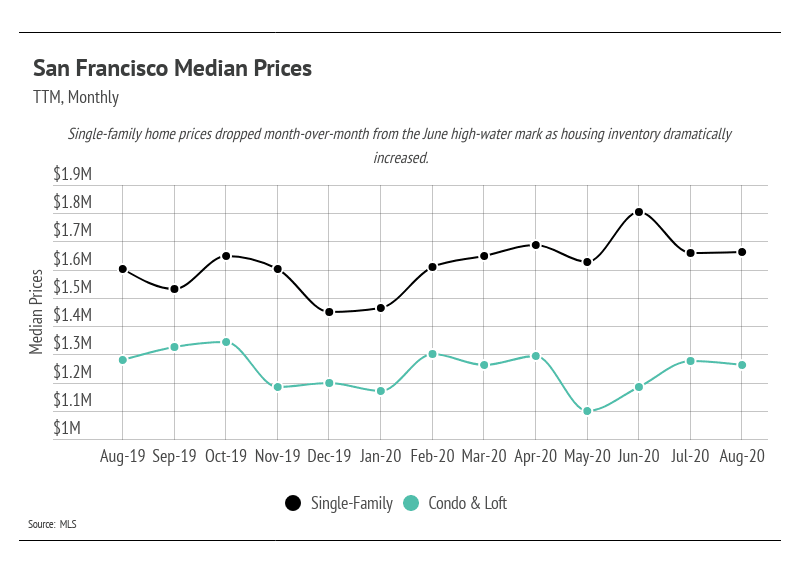

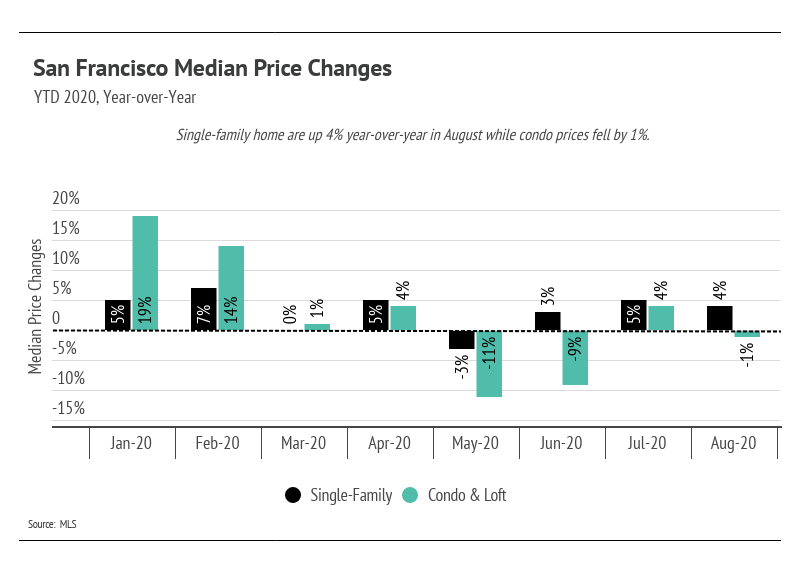

In August, single-family home and condo prices remained relatively unchanged despite more inventory coming to market.

Year-over-year, single-family home prices are up 4%, while condos are down 1%.

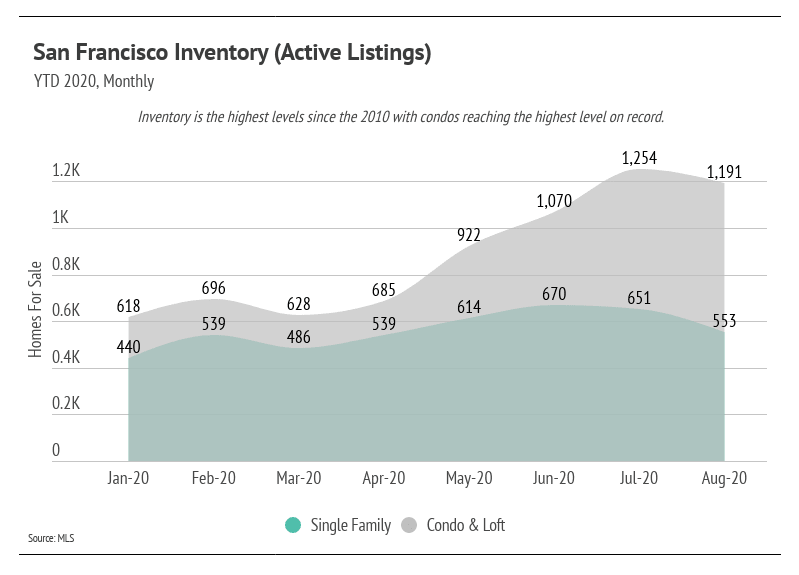

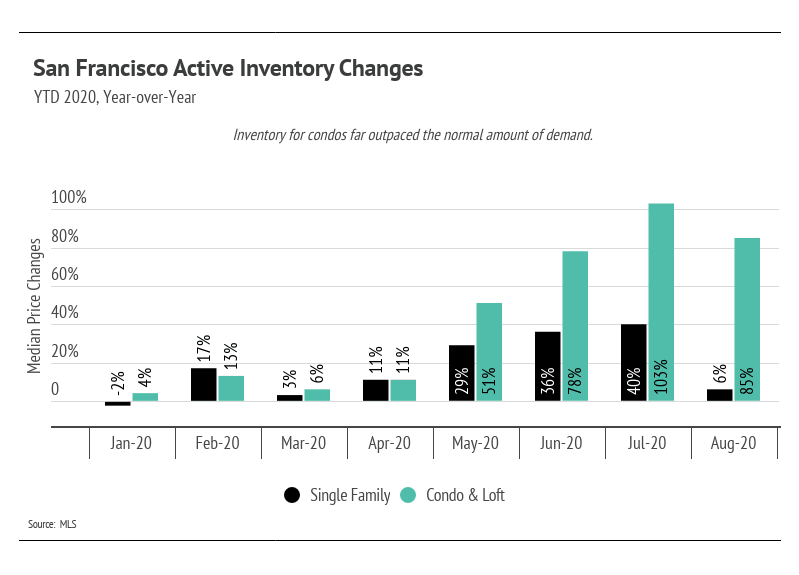

The inventory of homes for sale remains near its highest levels since 2010. Typically, a surge in supply would bring down prices; however, demand still outpaces supply even with the 40% year-over-year increase in active listings. Lack of supply compared to demand typically buoys San Francisco’s prices, which still remains true. We believe that the supply will make the market more efficient because buyers will have more options to find what they actually want, which will lead to more sales. San Francisco has needed more supply for quite some time, so we view the influx as a net positive for the market.

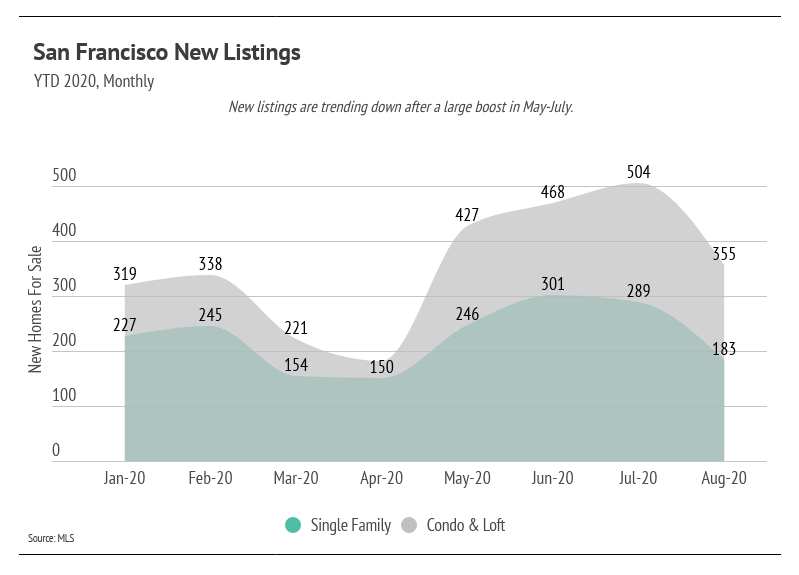

To fully appreciate the rise in inventory, we must look at how new listings and sales behaved in 2020. During the initial months of the pandemic (March and April), buyers and sellers hesitated to enter the market or entirely withdrew from it. Sellers, especially those with condos, began to reenter the market in May, driving up condo inventory. New listings for single-family homes increased in May and June, but were still below seasonal norms. With the current amount of active inventory, the decrease in new listings in August is a natural reaction to the oversupply.

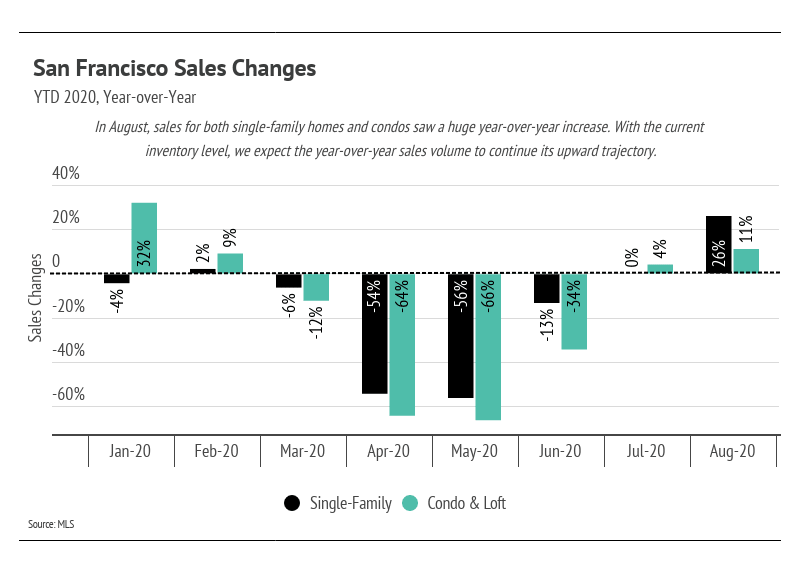

Home sales fell to their lowest levels since 2009 in April and May and were also down significantly in June. We’ve seen a large year-over-year sales increase in August, which is an amazing recovery from the lows in May. The increased inventory gives buyers a larger selection and greater ability to find the right home.

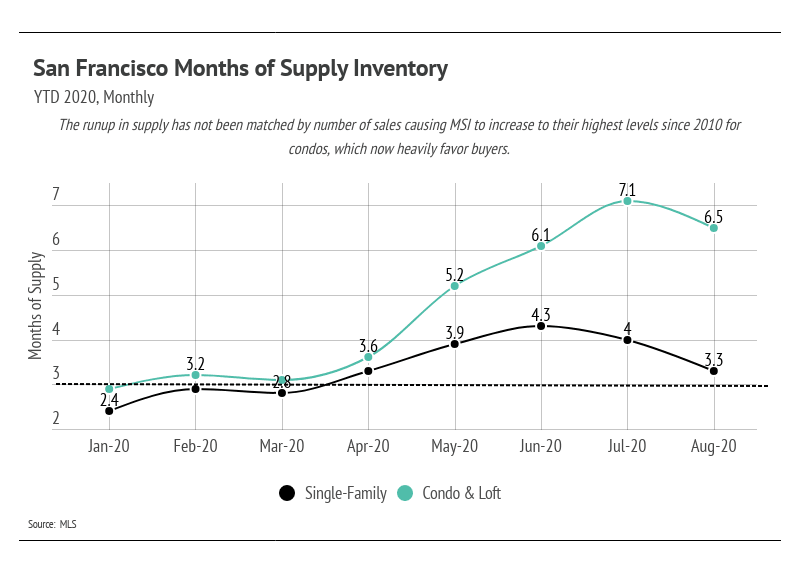

We can look to Months of Supply Inventory (MSI)—the measure of how many months it would take for all current homes for sale on the market to sell at the current rate of sales—as a metric to judge whether the market favors buyers or sellers. MSI has an average of three months in California, which indicates a balanced market. An MSI lower than three means that buyers are dominating the market and there are relatively few sellers, while a higher MSI means there are more sellers than buyers. In August, the MSI for single-family homes fell near the three-month mark indicating that the market is balanced, neither favoring buyers or sellers. The MSI of condos (around 6.5) was not as tight and clearly favors buyers; however, it is trending lower with the increase in sales.

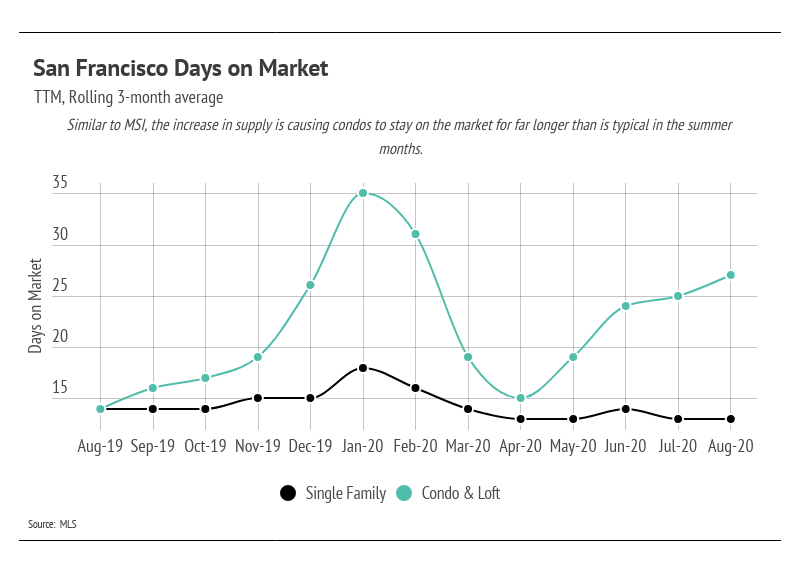

The Days on Market (DOM) for condos continued its upward trend through August, corresponding to the increased inventory, and is more in line with what we typically see in the winter season. Condos are taking longer to sell, which makes working with an agent that can differentiate the property and create a winning selling strategy even more important. DOM for single-family homes remains consistently low.

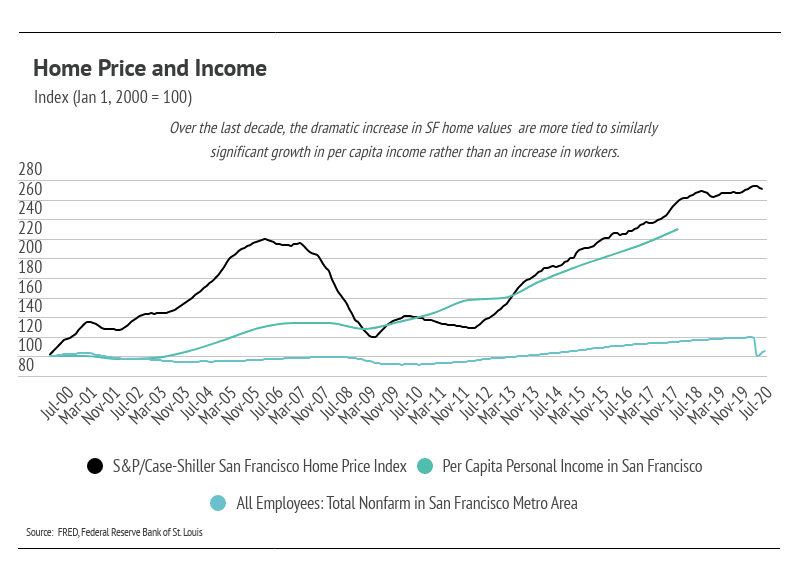

Home prices have remained steady despite a large boost in inventory, especially for condos, over the last several months. San Francisco, and California in general, tend to live in a constant state of undersupply, which elevates home prices. We often are able to explain home price fluctuation through supply and demand, but recent months point toward a third factor, Per Capita Income, which explains why the large increase in supply did not cause a similar drop in price.

We found that San Francisco home prices track much more similarly to per capita income rather than working population (as a proxy for potential home demand) as shown in the chart below. Per capita income illustrates why home prices don’t immediately fall when more inventory comes to market. Simply put: home values are supported by the overall wealth in the area.

Those unaffected financially by the pandemic likely have more money than expected without the usual travel and entertainment expenses. With more expendable income and low cost financing, we expect home prices to remain stable.

Moving forward, we anticipate new listings to slow until excess inventory lowers. Home prices will likely remain stable without outsized gains or losses year-over-year.

As always, we remain committed to helping our clients achieve their current and future real estate goals. Our team of experienced professionals are happy to discuss the information we have shared in this newsletter. We welcome you to contact us with any questions about the current market or to request an evaluation of your home or condo.

We’re here to help you and anyone you care about.

Stay up to date on the latest real estate trends.

BUSINESS

June 1, 2026

BUSINESS

May 1, 2026

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

BUSINESS

September 1, 2025

You’ve got questions and we can’t wait to answer them.