Note: You can find the charts & graphs for the Big Story at the end of the following section.

Another market slowdown

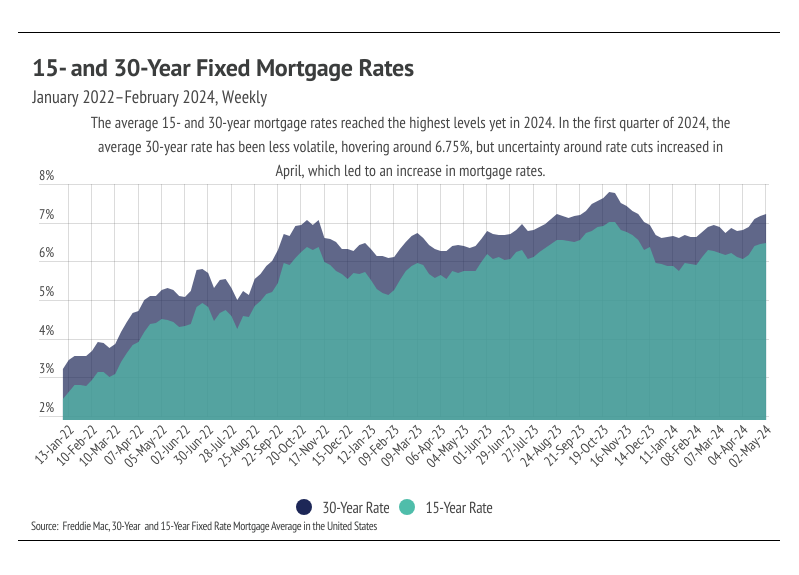

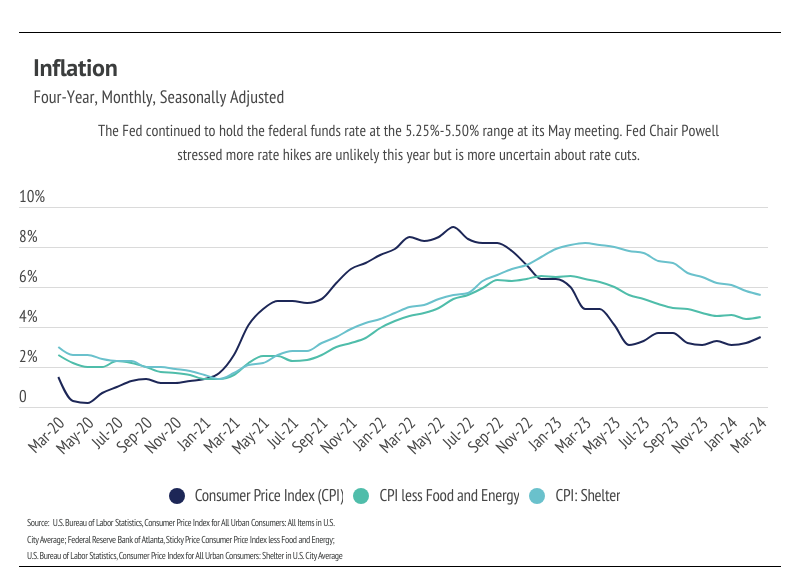

The average 30-year mortgage rate began the year at 6.62%, marking the start of the third year mortgage rates have been elevated. However, the rate expectations for 2024 in January were far different from those today. In January, inflation was still trending lower and economists were predicting rate cuts as early as March. Unfortunately, the inflation rate stopped falling around 3%, never quite reaching the 2% target, which has caused the Fed to delay cutting the federal funds rate, which indirectly, but significantly, influences credit markets. The past two months, in fact, inflation has increased year over year, which isn’t ever going to move the timetable for rate cuts earlier.

During its May meeting, the Federal Reserve unanimously voted to hold policy rates steady for the sixth consecutive time, leaving the federal funds target rate unchanged at 5.25% to 5.50%. Importantly, Fed Chair Jerome Powell emphasized that it’s unlikely that the next policy rate move will be a hike; it’s more likely that rates remain steady and with less clarity of cuts. The Fed’s dual mandate aims for stable prices (inflation ~2%) and low unemployment. The jobs market is still strong, so really, it’s all about inflation.

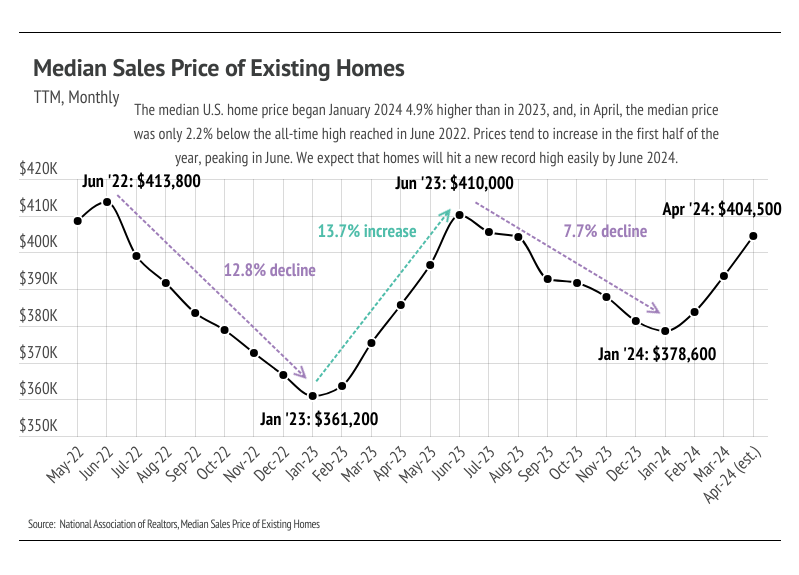

The Fed’s change of tune has led to much higher mortgage rates. Mortgage rates have risen 0.6% since the start of the year, and two thirds of that increase happened in April. Rising rates, especially quickly rising rates, only slow the housing market. As we entered May, the average 30-year mortgage rate hit 7.22% — the highest level in 2024 and not too far off from the 23-year high of 7.79% hit last year. During April, prices and rates increased, thereby decreasing affordability. For buyers planning to finance a home, the 0.38 percentage point increase that occurred in April affects the monthly cost of a home dramatically. When we couple the median price increase with the mortgage rate increase in just the month of April, the monthly cost increased 7%. If we compare the month cost in January to April, the monthly cost rose 13%.

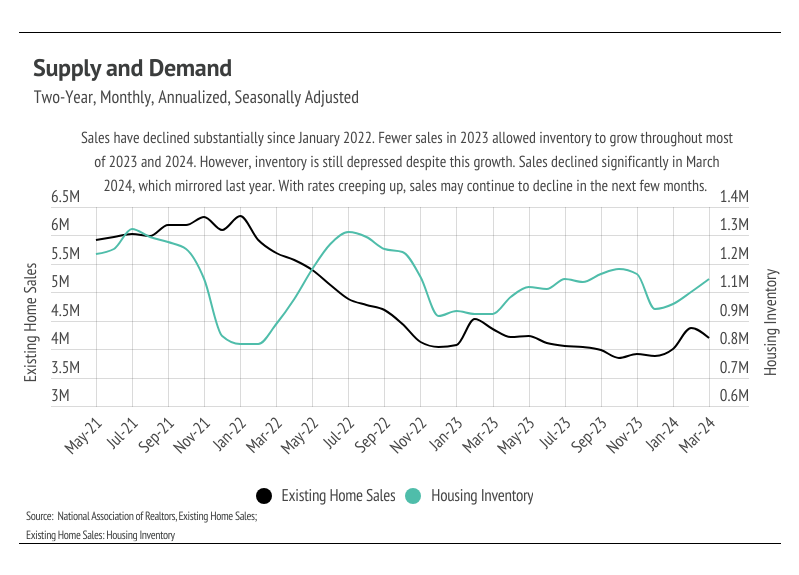

Rates seem to be able to inflate prices and increase sales when they’re low, but when they’re high, they only slow sales — or, at least, that’s been the experience over the past four years. Inventory is, of course, driving the disconnect. Demand is still high relative to supply, even though inventory is growing. However, as prices increase, the buyers who haven’t been priced out of the market become pickier, and fewer but pickier buyers creates an overall slowdown. The market was showing signs of a more normal spring with sales and inventory rising, but the recent rate increases dropped sales last month, which is almost never seen in the spring. Even though mortgage rates have been elevated for long enough that it feels more normal, mortgage rates above 7% will naturally give potential buyers and sellers pause before entering the housing market.

Different regions and individual houses vary from the broad national trends, so we’ve included a Local Lowdown below to provide you with in-depth coverage for your area. As always, we will continue to monitor the housing and economic markets to best guide you in buying or selling your home.

Big Story Data

The Local Lowdown

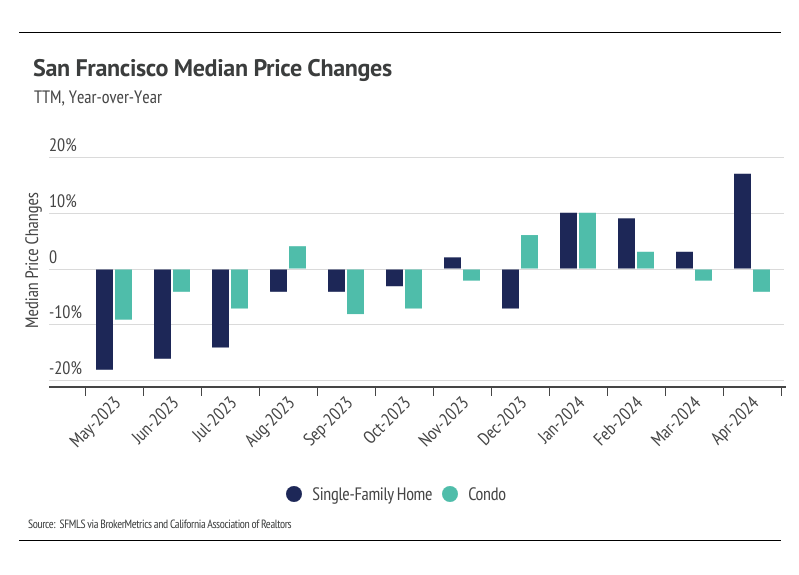

Median single-family home and condo prices rose meaningfully from December 2023 to April 2024, up 27.6% and 10.6%, respectively. Year-over-year prices also appreciated for single-family homes, up 16.5%

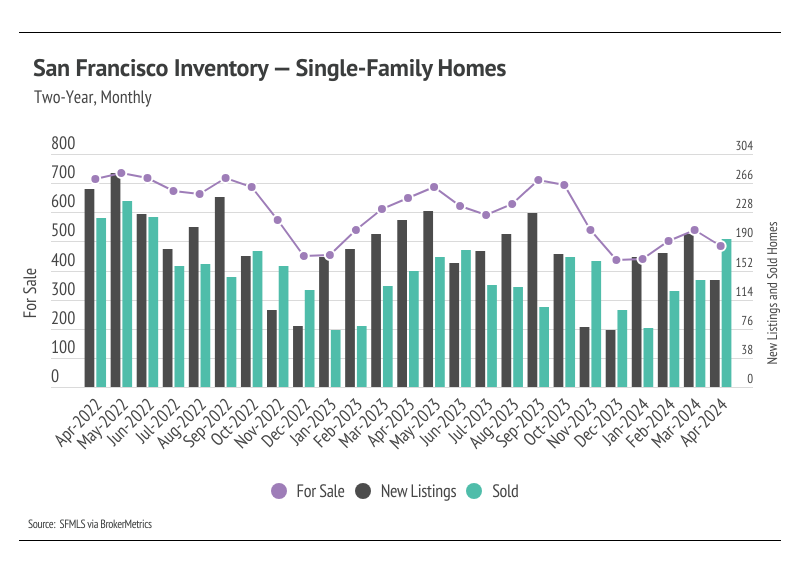

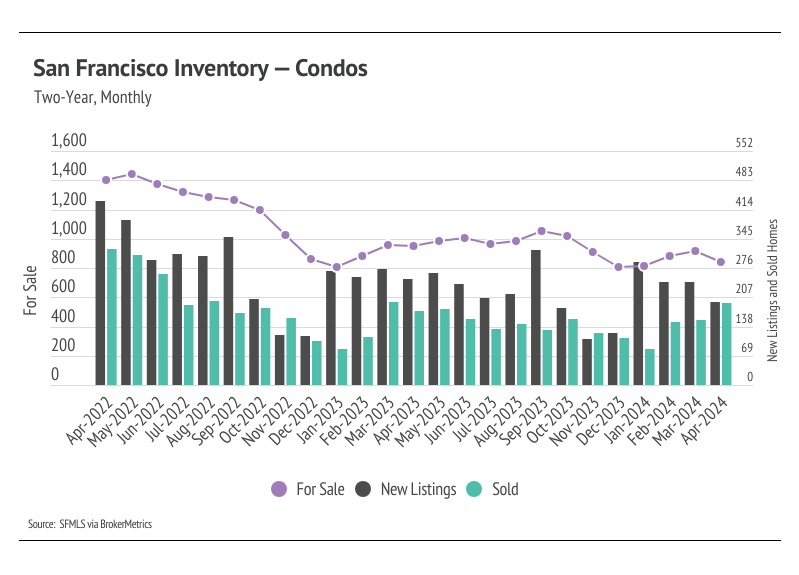

Active listings in San Francisco fell 7.6% month over month. Both single-family home and condo inventory are once again near record lows, as sales increased and new listings fell.

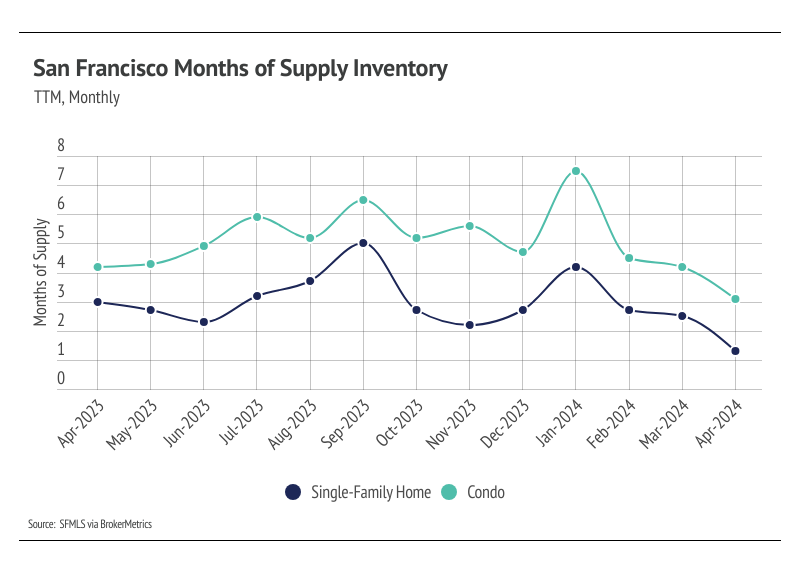

Months of Supply Inventory fell from January to April 2024, indicating that buyer competition is ramping up. MSI implies a sellers’ market for single-family homes and a balanced market for condos.

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

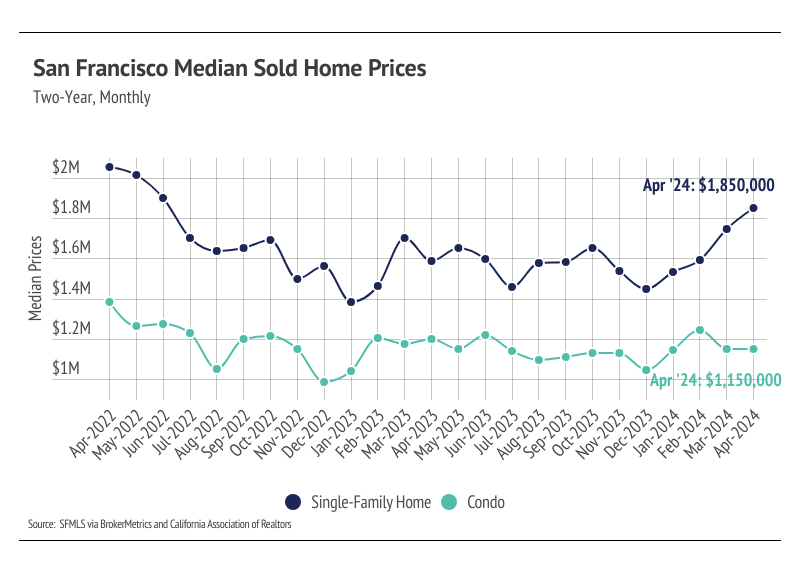

The median single-family home price rose significantly in April 2024

In San Francisco, home prices haven’t been largely affected by rising mortgage rates after the initial period of price correction from May 2022 to July 2022. Since July 2022, the median single-family home and condo prices have hovered around $1.5 million and $1.2 million, respectively. However, for single-family homes that trend may be changing. From December 2023 to April 2024, the median single-family home price rose significantly, up 28%. Year over year, the median price rose 17% for single-family homes, but fell 4% for condos. We expect prices to rise as more sellers come to the market. Additionally, inventory is so low that rising supply will only increase prices as buyers are better able to find the best match. More homes must come to the market to get anything close to a healthy market.

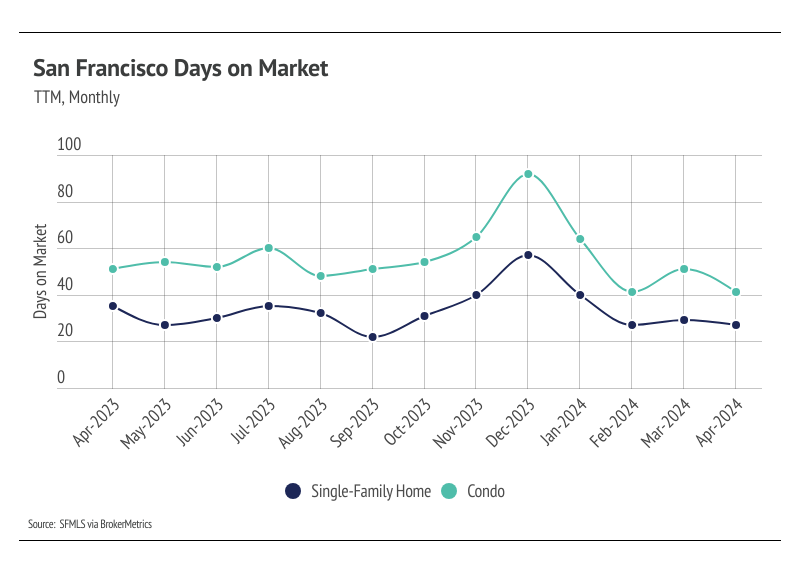

High mortgage rates soften both supply and demand, but homebuyers seemed to tolerate rates above 6%. Now that rates are above 7%, sales may slow slightly in the next couple of months, which isn’t great for the market, but isn’t it terrible, either, as it may allow inventory to build in a massively undersupplied market.

Single-family home and condo inventory fell, but sales increased dramatically month over month

Since the start of 2023, single-family home inventory has followed fairly typical seasonal trends, but at a significantly depressed level, while condo inventory has been in decline since May 2022. Low inventory and fewer new listings have slowed the market considerably. Typically, inventory peaks in July or August and declines through December or January, but the lack of new listings prevented meaningful inventory growth. Last year, sales peaked in May, while new listings and inventory peaked in September. New listings have been exceptionally low, so the little inventory growth throughout the year was driven by fewer sales. In November and December 2023, new listings dropped significantly without a proportional drop in sales, causing inventory to fall to an all-time low in December, which further highlights how unusual inventory patterns have been over the past year. However, new listings in January 2024 rose 134% month over month.

The number of new listings coming to market is a significant predictor of sales, and the new listings in January led to a 68% sales increase in February. Both inventory and new listings declined from March to April, but sales rose considerably, up 33%. Year over year, inventory is down 16% and new listings are down 25%, but sales are up 20%. Demand is clearly coming back to San Francisco, but more supply is needed for a healthier market.

Months of Supply Inventory in March 2024 indicated a sellers’ market for single-family homes

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes listed on the market to sell at the current rate of sales. The long-term average MSI is around three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). The San Francisco market tends to favor sellers, at least for single-family homes, which is reflected in its low MSI. However, we’ve seen over the past 12 months that this isn’t always the case. MSI has been volatile, moving between a buyers’ and sellers’ market throughout the year. From January to April, MSI declined significantly, indicating that single-family homes shifted from balanced to favoring sellers, and condos moved from favoring buyers to balanced.

Local Lowdown Data

--------------------------

If you are interested in selling, buying or just curious about the

San Francisco and Bay Area real estate market, please give me a call.

We are here to help you and anyone you care about.

--------------------------