SAN FRANCISCO REAL ESTATE MARKET UPDATE – January 2022

January 6, 2022

BUSINESS

January 6, 2022

BUSINESS

Quick Take:

Note: You can find the charts & graphs for the Big Story at the end of the following section.

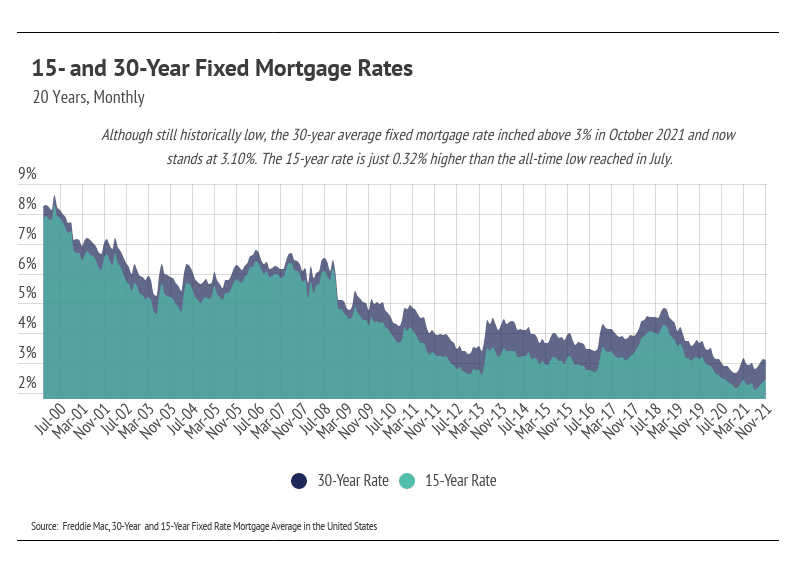

Although not necessarily a strict supply chain issue, the rising cost of housing can definitely be tied to supply. In the U.S., the supply of houses for sale is still near the all-time low reached in April. At the same time, demand remains high for homes, and we are on pace to have around a million more homes sold in 2021 than in a typical year, based on the long-term average. In other words, more homes are selling despite the historically low inventory. Because inflation diminishes the purchasing power of a dollar over time, buyers face pressure to buy sooner rather than later, further increasing demand for homes. Coupling inflation with historically low mortgage rates creates incentives to buy now even with the run-up in prices.

The market remains competitive for buyers, but conditions are making it an exceptional time for homeowners to sell. Low inventory means sellers will receive multiple offers with fewer concessions. Because sellers are often selling one home and buying another, it’s essential that sellers work with the right agent to ensure the transition goes smoothly.

_________________________

Quick Take:

Note: You can find the charts/graphs for the Local Lowdown at the end of this section.

_________________________

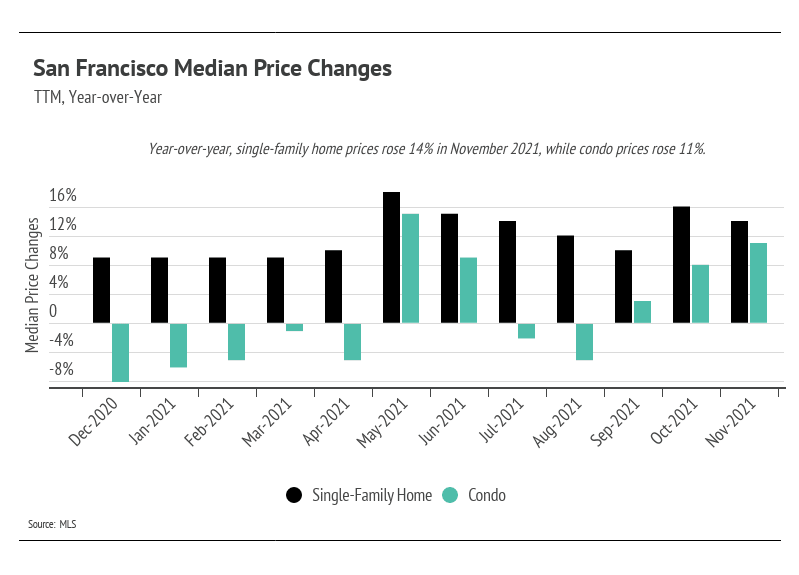

After single-family home prices appreciated significantly in the first half of the year, it made sense that we would see a correction in the third quarter. Prices rebounded in the fourth quarter, moving higher but below peak levels. Sales jumped the past two months, causing prices to climb higher, just under peak.

Condo prices, however, reached an all-time high in November. This is the first new high we’ve seen in over a year. The pandemic hit demand for condos hard, but price and sales indicate that demand is back.

_________________________

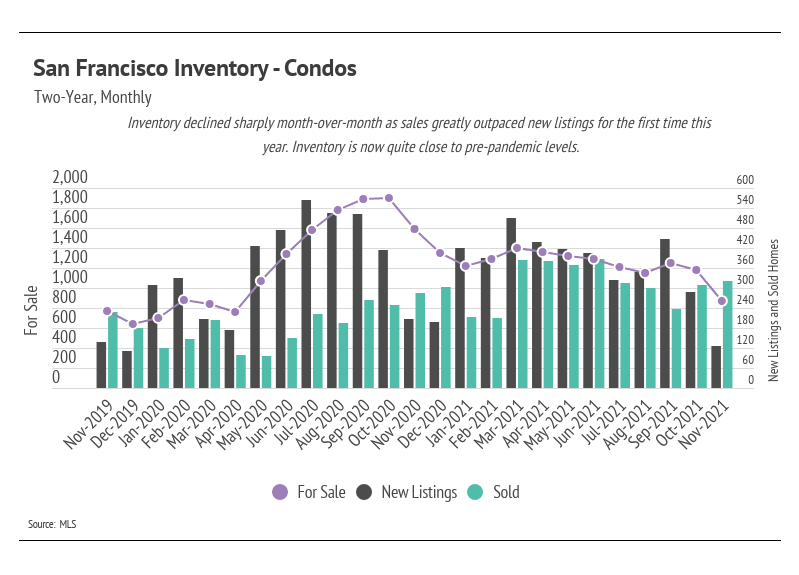

Despite the slight increase in a single-family home and condo inventory in 2021, we’re still at a historic low. August and September are typically the months each year with the highest inventory. In 2021, total inventory didn’t come close to last year’s level. Even though we’re seeing some price correction after the first half of the year for single-family homes, the sustained low inventory will lift prices. Sales in San Francisco have been incredibly high, again highlighting demand in the area.

_________________________

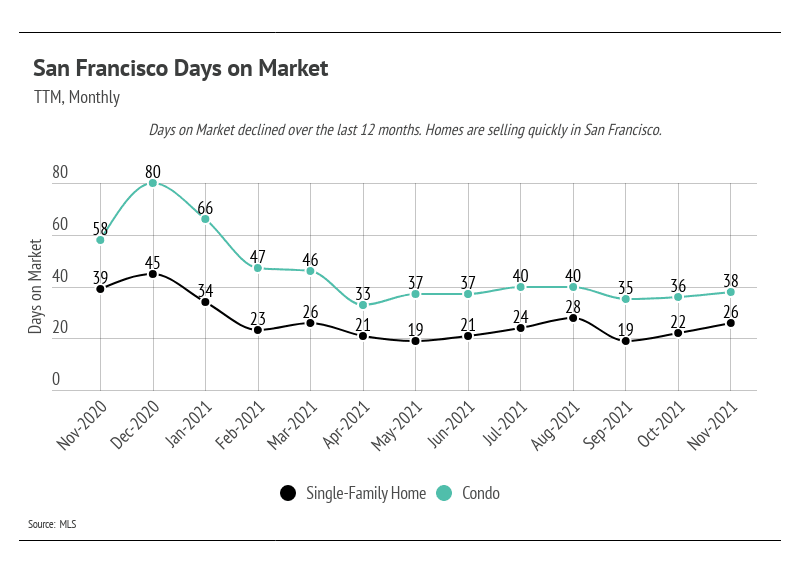

Homes are selling faster than at any point in the past 15 years. The Days on Market reflects the high demand for homes in San Francisco. Buyers must put in competitive offers, which, on average, are 16% above the list price for single-family homes and 4% above for condos.

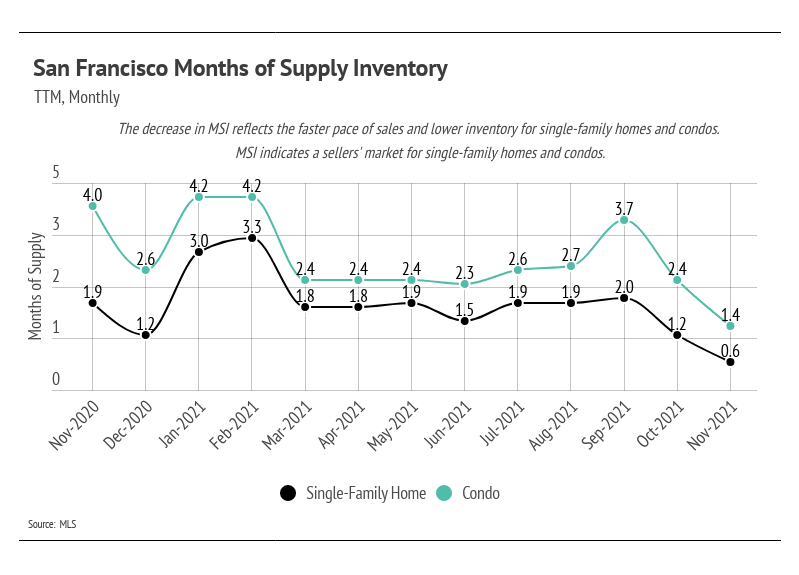

Months of Supply Inventory (MSI) quantifies the supply/demand relationship by measuring how many months it would take for all current homes for sale on the market to sell at the current rate of sales. The average MSI is three months in California, which indicates a balanced market. An MSI lower than three indicates that there are more buyers than sellers on the market (meaning it’s a sellers’ market), while a higher MSI indicates there are more sellers than buyers (meaning it’s a buyers’ market). Currently, single-family home and condo MSIs are both low, indicating a sellers’ market.

_________________________

Stay up to date on the latest real estate trends.

BUSINESS

May 1, 2026

BUSINESS

April 1, 2026

BUSINESS

March 1, 2026

HELM Newsletter

February 1, 2026

BUSINESS

January 1, 2026

BUSINESS

December 1, 2025

BUSINESS

November 1, 2025

BUSINESS

September 1, 2025

BUSINESS

August 1, 2025

You’ve got questions and we can’t wait to answer them.